Introduction and Theory

Scholars have long realized that economic leverage can be a powerful tool in international relations, whether used as a ‘stick’ or ‘carrot.’ 1 However, most of the existing literature on economic sanctions is rooted in the implicit assumption that a few wealthy states—the United States (U.S) and its Western allies—will be able to impose sanctions with impunity on smaller, weaker states. Almost all of the classic cases considered in the sanctions literature are of this type, focusing for example on sanctions by the U.S. and Europe against North Korea, Cuba, South Africa in the Apartheid era, Iraq under Saddam Hussein, and Yugoslavia under Slobodan Milosevic. 2 While the literature has innumerable studies of these cases, sanctions by non-Western actors are much more rarely considered. For example, this bias is seen even the most authoritative study of sanctions (Hufbauer, et.al., 2007). This work focuses on 174 cases of sanctions since 1914. Yet over two-thirds of the cases chosen involve the U.S. as initiating country (118 out of 174). When cases initiated by the E.U. countries are included, we see that 145 of 174 cases (over 83%) are Western-based. The main focus of this literature has been on how the sanctions can be made more effective. How can other Western countries and the United Nations (UN), be induced to support sanctions? Can the sanctions be made ‘smart,’ by better targeting of vulnerable economic sectors and key leaders (Cortright & Lopez 2002)?

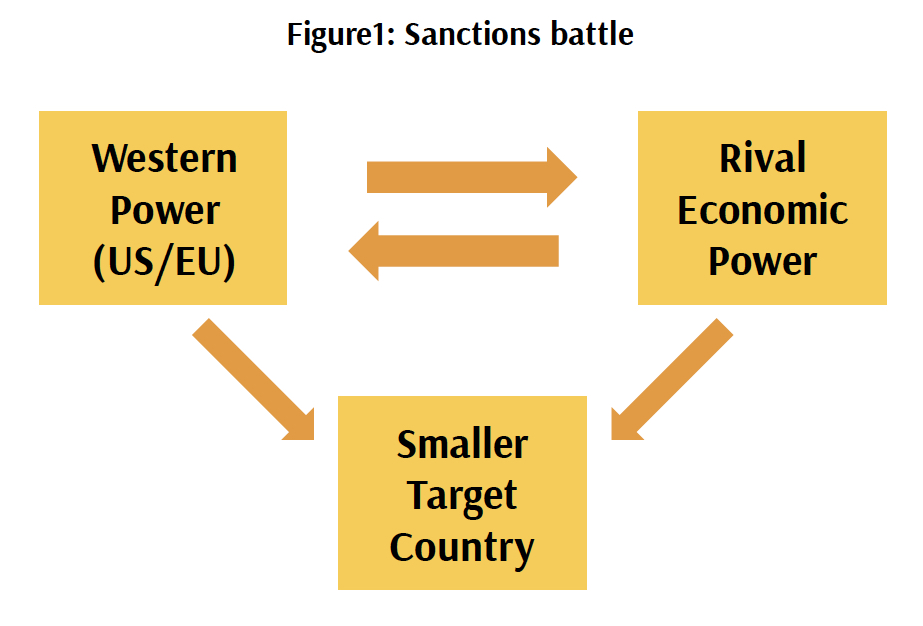

This casual assumption of Western economic hegemony ignores some of the lessons of history. For example, before the Second World War, countries such as Nazi Germany and Imperial Japan represented formidable adversaries, not only for their military might but for their economic power, which enabled them to manipulate their neighbors and to fight back against Western sanctions.3 Even during the Cold War, although the Soviet Union and its allies clearly had less economic clout than the West, they could still use economic aid and trade to try to counter Western policies.4 Today, as the world again becomes more multipolar, we can no longer focus on only unidirectional sanctions with the West targeting isolated, weak countries. Authors such as Blackwill and Harris (2016) have made it clear that the new era of ‘geoeconomics’ will be much more challenging. States such as China (now the world’s second largest economy) and Russia (one of the world’s largest oil and gas producers) clearly have the economic clout to resist Western sanctions—and impose sanctions of their own, both against weaker target states and against the West itself. Thus, as in the Ukrainian case, analysts may have to consider up to four distinct strands of sanctions (see Figure 1). The West may be targeting a small state with either aid or sanctions, and a strong economic rival may be targeting that state as well. Yet at the same time, the two larger powers may be sanctioning each other.

How can we best evaluate the effectiveness of sanctions? Even for a single strand of sanctions this remains controversial, let alone for multiple conflicting sanctions. Some in the literature argue that sanctions rarely work while others see them as very useful.5 Sanctions advocates like David Baldwin (1986) have long pointed out that harming the target state economically is a form of success. Yet even this effect is not always easy to measure. Perhaps the most obvious indicator of economic impact would be an overall decline in the country’s Gross National Product (GNP). Yet this may not be obvious in the short term, and may be caused by many other factors. One can also look at measures such as the target state’s trade and capital flows and the value of its currency and stock market.

However, even if sanctions do cause economic pain, they may not result in political compliance by the target state. The classic study by Hufbauer et al. (2007) estimates that, at most, only one third of sanctions attempts result in compliance. And if a state does change its policies, it will have a large incentive to deny that the change has resulted from foreign pressure, since it does not want to appear weak. As we shall see, there is a lively debate on whether the West’s sanctions against Russia in the Ukrainian case have had any real impact on the Kremlin’s policies.

One problem for the West, then, is that it may now face a more complex world, where multiple sanctions must be evaluated, since hostile, economically powerful states can counter Western sanctions with their own. However, a second problem for the West should also be of concern. Different types of governments respond differently to sanctions. For example, scholars have noted that democratic regimes may be more vulnerable to economic pressure than non-democratic ones (Lektzian & Souva 2007). Democratic leaders must listen more to public opinion, and must fear losing elections if the public turns even slightly against them. One of the most well-documented theories in Political Science is the economic theory of elections. Many studies have shown that if a country’s economy falls by 1%, the vote share of an incumbent leader will decline by about 2% (Markus 1988; Bartool & Sleg 2009). This fact sometimes works to the West’s advantage—if it is trying to sanction a state with competitive elections. Such has been the case with Iran, which agreed to curb its nuclear ambitions in large part because of sanctions (Newnham 2011a). Its current leader, Hassan Rouhani, is well aware that a major reason for his election was public anger with economic stagnation due to sanctions, and he thus had a mandate to change Iran’s foreign policy. However, the West generally is trying to sanction authoritarian regimes, which can only be overthrown when popular anger is much greater. The ‘cost’ of opposing Vladimir Putin in Russia is much higher for an average citizen than the cost of voting against Rouhani in Iran, or Barrack Obama or Donald Trump in the U.S. This could be a problem for the West in the Ukrainian case. Both Ukraine and the Western countries themselves, as democratic states, may be more vulnerable to sanctions than Russia.

Also, authoritarian leaders, with their control over the news media, may be better able to provoke what is known as a ‘rally "round the flag"’ effect (Galtung 1967; Eland 1995). If a country is being sanctioned, the public may ignore economic hardship and, in a burst of patriotism, support national leaders even more strongly, at least in the short term. As we shall see, this seems to have happened in Russia after Western sanctions were introduced, which will make it difficult for Western sanctions against Moscow to be effective in the immediate future.6

This paper will proceed as follows. First, I will try to evaluate the power of Western economic leverage. Of course, a key focus will be sanctions against Russia which have been rolled out in several phases starting in spring 2014. However, it must be remembered that the West, like Russia, has sought for years to use both sanctions and incentives to influence Ukraine. Thus, the ‘economic battle for Ukraine’ in fact began well before the outbreak of the current crisis. Next, I will consider Russia’s economic power and its impact. Russia has long tried to use its economic strength to win over Ukraine. For years it has offered various forms of economic aid to pro-Russian leaders there, while punishing pro-Western governments. This pattern escalated greatly as the present crisis unfolded. By summer 2014, as the West began to sanction Russia, the Kremlin retaliated with its own economic attacks on the U.S. and its allies. Finally, the paper will attempt to draw some conclusions and will present policy recommendations.

Western Economic Power and Ukraine

Most outside observers noticed the ‘economic war for Ukraine’ only in the spring of 2014, when the West began to impose sanctions on Russia after its armed intervention in the Crimea. However, in fact the U.S. and the European Union (E.U.) have been working to promote their agenda in Ukraine for some time. Perhaps most notably, the E.U. has long included Ukraine on its list of Eastern partners, steadily forging closer ties with Kyiv. This has encouraged pro-Western forces in the country to dream of eventual E.U. membership, although that prospect still seems distant. The E.U. first signed a Partnership and Cooperation Agreement with Ukraine in 1994 and followed up by including the country first in its Neighborhood Policy and then in the deeper Eastern Partnership in 2009.

The E.U.’s efforts represented a substantial economic incentive to Ukraine to look to the West. If full E.U. membership could be achieved, Ukraine could benefit from the large, wealthy E.U. market for its agricultural and industrial goods. Its people could study and work in the E.U., where salaries are vastly higher. The country could qualify for a cornucopia of E.U. subsidies and grants.7 Kyiv would receive administrative help, to improve government efficiency and cut corruption. The E.U. companies would be encouraged to invest in Ukraine, taking advantage of lower salaries and underused factories while still being able to produce within the E.U. zone.8

The potential impact of these changes can be seen dramatically just across the country’s Western border. Poland and Ukraine had roughly the same standard of living when Communism collapsed in Eastern Europe 25 years ago. Now, however, over ten years after joining the E.U., Poland’s per capita GNI (Gross National Income) is almost four times that of Ukraine.9 Recent historical memories make this comparison all the more striking for those living in Western Ukraine. The Galicia region, for example, centered on Lviv, was linked to Poland for centuries. It was part of the Polish-Lithuanian Commonwealth, then the Austro-Hungarian Empire, and finally interwar Poland until 1939. After Ukrainian independence it was only natural for many in that country to look with envy at the surging growth across the nearby border.

In fact, it was the power of the E.U.’s economic influence that precipitated the current international crisis over Ukraine. President Victor Yanukovych, considered friendly to Moscow, found the lure of the E.U. ties so irresistible that he surprisingly agreed to an Association Agreement with the Union, which was to be signed in November 2013. When threats and economic pressure from Moscow forced him to back out of signing the pact, pro-Western demonstrations erupted that eventually led to his downfall in February 2014. Not surprisingly, those demonstrations featured many Western Ukrainians, especially those from the Lviv region.10 The political impact of the E.U. was dramatized when the protesters christened their demonstration on Maidan Square in Kyiv as “Euro-Maidan” and adopted the E.U. flag as their symbol. The West increased the pressure on Yanukovych by threatening sanctions against his top associates: the U.S. imposed visa bans, and on February 21, 2014, just before the Ukrainian government fell, the E.U. imposed both visa bans and asset freezes (2014, ‘EU imposes Ukraine sanctions after deadly Kiev clashes,’ BBC News, 21 February).

With the fall of Yanukovych and the installation of a pro-Western provisional government both the E.U. and U.S. moved to deploy economic instruments to help Kyiv’s beleaguered rulers. The E.U. quickly announced, in April 2014, that more Ukrainian products would be allowed into the E.U. duty-free (Regulation EU no. 374 2014). The E.U. also signed the delayed Association Agreement with the new Ukrainian government on June 27, 2014. It contained a Deep and Comprehensive Free Trade Agreement which Kyiv hoped would help it to reorient its trade away from Russia.11 Both the E.U. and U.S. also announced financial support for the struggling Ukrainian government. The E.U. quickly offered a package of 11 billion euros. The International Monetary Fund (IMF) stepped forward with another $17-18 billion in financing (European Commission 2014; Mayeda 2015). This aid was partly intended to cushion the country from considerable economic blows from Russia, which will be detailed below. The Ukrainian government at the time was pinning its hopes for survival on an economic reorientation toward the West. This was evident in President Poroshenko’s selection of Aivaras Abromavičius, a Lithuanian citizen, as his Minister of the Economy, an American, Natalie Jaresko, as his Finance Minister, and the pro-Western former leader of Georgia, Mikheil Saakashvili, as Governor of the Odesa region. However, the efforts of Poroshenko and the West did not pay off immediately: the World Bank estimated that the Ukrainian GDP may have fallen by up to 12% in 2015, after a 7% fall in 2014, and inflation peaked at 61% in mid-2015 (World Bank 2015). There was a modest recovery in 2016, with a 2% rise in GNP, but the country remains in deep economic trouble. Overall, then, the West’s aid to Ukraine may have helped to win the country to its side politically—but has not, at least yet, succeeded in healing its economy.

Western Economic Power and Russia

While the U.S. and the E.U. worked to strengthen the new pro-Western government in Kyiv, Russia intervened against Ukraine using both military and economic instruments, as will be detailed later in this article. This, in turn, led the West to open a new front in the economic battle for Ukraine—sanctions against Moscow. Thus far there have been three major rounds of sanctions. And there may be more. At the G-7 summit in Germany in June 2015, the assembled leaders agreed to plan further sanctions if Moscow did not halt its interference in Eastern Ukraine. The summit’s final communiqué warned that 'we stand ready to take further restrictive measures in order to increase the cost to Russia should its actions so require' (Carter & Cole 2015).

The E.U., the U.S., and their partners have thus far employed similar, coordinated sanctions against Moscow. Throughout this effort, these powers have been at pains to follow the careful 'smart sanctions' approach advocated by authors such as Cortright and Lopez (2002) and Maureen O’Sullivan (2003). Many noted the disastrous social consequences of the wholesale sanctions against Iraq from 1990-2003. Forbidding Iraq to export oil impoverished the country, leading to negative consequences such as spikes in infant mortality. Furthermore, the experts believed, such wholesale sanctions—as also practiced for years against North Korea and Cuba—merely angered the target state’s population, driving them closer to their rulers. Thus the sanctions against Moscow seemed designed to reduce ‘collateral damage.’ Instead of banning a major Russian export or denying Russia large-scale imports—measures which would hurt whole areas of the Russian economy and also hurt the profits of many Western firms—the West turned first to targeted financial sanctions against companies and individuals closely associated with President Putin. These were gradually expanded to sectoral sanctions against financial and energy firms.

The first round of sanctions, announced in March 2014 when Russia began its incursion in Crimea, was quite limited. The West suspended ongoing talks on increased economic cooperation with Russia. Some individuals involved in the Crimean operation were targeted. The U.S. initially issued travel bans and asset seizure orders for 11 individuals, while the E.U. targeted 21, many of them lower-ranking (Myers & Baker, 2014). In addition to punishing these individuals, it was hoped that two more effects would make themselves felt. First, the measures might help induce those targeted to begin to quietly lobby President Putin to mend his ways. Second, Washington and Brussels hoped that, despite the small size of the initial sanctions, they would frighten risk-shy investors, weakening Russia’s currency, stock market, and overall investment climate.

When Russia moved beyond the Crimea and began to support secessionist forces in Eastern Ukraine, a second round of sanctions went into effect in late April. This lengthened the list of targeted individuals, including such prominent names as Igor Sechin, the Chairman of Russia’s most valuable oil company, Rosneft. It also went beyond individuals for the first time, adding some Russian corporations and banks that were seen as especially close to President Putin’s inner circle, such as Rostec, SMP Bank and InvestCapital Bank (Baker 2014).

Finally, in the summer of 2014, the West moved to a third round of sanctions. By now Putin’s support for the Donbas rebels had become clearer, and the West was especially revolted when the rebels downed a Malaysian jetliner over the conflict zone, killing almost 300 innocent civilians—over two-thirds of them from the E.U. Accordingly, in July the West added a number of names to the list of those facing individual sanctions, and also added several important Russian banks (Sberbank, VTB Bank, Russian Agricultural Bank, Gazprombank and Vneshekonombank) and state-owned oil companies (Rosneft and Novatek). The export of any dual-use technology to Russia was prohibited. And for the first time whole sectors of the Russian economy were targeted, albeit in a limited way. For example, it was agreed that certain kinds of oil-drilling equipment could not be shipped to Russia and that new Western investment in that sector should be limited (Borger, Lewis & Mason 2014).

However, Russia not only persisted in aiding the Donbas rebels, it intervened in the conflict with its own army—albeit in a still ‘masked’ way, with Russian tanks being marked with the flag of ‘Novorossiya,’ for example. Russia’s action, at the end of August, turned what had seemed a likely victory for Kyiv in the disputed region into a rout. Accordingly, in September the West reacted by tightening sanctions still further (Council of Europe 2014). Finally, with the weakening of the September 2014 Minsk ceasefire agreement in late 2014, the West moved to add still more sanctions. While a large new ‘fourth round’ was not yet forthcoming, the E.U. did add some additional names to the list of sanctioned individuals in January 2015 and announced that further measures were being studied (2015, ‘Ukraine conflict: E.U. extends sanctions against Russia,’ BBC News, 29 January). Since then, the sanctions have been renewed every six months. While the Trump administration is widely viewed as less sympathetic to the sanctions, thus far it has not changed them.

Evaluating the Effects of Western Sanctions

Have the West’s sanctions against Moscow been successful? In examining this key question, several aspects of the sanctions’ impact should be considered: first, their effect on the target state’s foreign policy actions. Second, their effect on its economy. And third, their effect on its domestic politics.

Some would argue that the sanctions have had little impact on the Kremlin’s foreign policy. Russia continues to keep a firm hold on Crimea and to assist rebels in Eastern Ukraine. Others argue that the current sanctions—and fear of yet stiffer penalties in the future—have helped to press Russia toward a diplomatic solution. They note that the Kremlin was very reluctant to commit its own forces in Eastern Ukraine, instead long preferring to merely aid weak local rebels—a strategy which came very close to failure in August 2014, when the Ukrainians nearly wiped out the insurgency. And when Russia did briefly intervene itself, to save the rebels from defeat, it was very quick to ask for a ceasefire and withdraw most of its forces—and at least in part, sanctions supporters say, to forestall further sanctions. President Putin was probably correct to say, in a controversial phone call with the President of the European Commission, José Barroso, 'if we want to, we can take Kyiv in two weeks' (Roth 2014). Yet instead, the Kremlin has largely contented itself with protecting the small rebel areas in the East, in effect—one could argue—conceding the rest of the country to the West. As we shall see below, another indication of the success of Western sanctions is the fact that Russia has felt compelled to resort to costly and controversial measures to counter them, including embargoes on Western food imports and a law to compensate wealthy oligarchs who were harmed by the sanctions.

While the impact of sanctions on Russian foreign policy may still be debatable, sanctions supporters can point to greater effects in the second area mentioned above—the Russian economy. These economic consequences have been sharply increased by the fortuitous timing of a major downturn in global oil prices, Russia’s main export. From June 2014 to January 2015 the price fell from about $110 to $50 per barrel. It then fell even lower, reaching $32 in early 2016, before stabilizing at around $50. Agencies such as the IMF have downgraded their predictions for Russia’s growth rate several times. After three rounds of sanctions, the IMF was predicting by fall 2014 that Russia would grow at most by 0.2% for that year. In October the E.U. projected that Russia would lose 1.1% in growth due to the sanctions in 2015, after losing 0.6% in 2014 (Norman 2014). Later forecasts were even more negative, as the slowdown has accelerated. A more recent estimate by the World Bank was that the country’s GNP fell by 3.8% in 2015 and would decline by a further 1-1.5% in 2016 (Razumovskaya 2016).

In the short term, the sanctions helped induce capital flight, with both foreign investors and Russians transferring funds out of the country. It was estimated that about $150 billion left the country in 2014, a serious burden when one considers that the total value of the Russian economy is about $2 trillion. This was double the figure for 2013 (2015, ‘Russia capital flight surges,’ Eurasianet). While that drain slowed in 2015, new investment essentially stopped. Russia’s anti-Western countermeasures, discussed below, have only accelerated the process. Why, for example, would McDonalds want to continue to invest in a country which arbitrarily closes its restaurants for "health violations" whenever there are political tensions between Washington and Moscow? (Matlack 2014). The same obviously applies to Western media companies, who are now being told they can own only 20% of any Russian media property (Sonne 2014). This is to say nothing of Western oil companies, who—because of the nature of their business—must commit vastly larger sums for a very long time period. Even in areas where sanctions permit investment, fears of future sanctions or Russian retaliation have effectively cut off financial flows. Net Foreign Direct Investment has plunged. World Bank figures show that Russia had net FDI inflows of $69.2 billion in 2013, $22 billion in 2014, and only $6.9 billion in 2015 (‘World Development Indicators Databank: Russia,’ The World Bank). This will have a real effect on the Russian economy in the medium and longer term.

A range of other indicators confirm the gloomy outlook for the Russian economy after sanctions were imposed. The rating of Russia’s sovereign debt was steadily downgraded, reaching ‘junk’ status in early 2015. This not only raises the country’s cost of borrowing, it also forces many investment funds to sell Russian bonds, as they are not permitted to hold non-investment grade bonds (Korb & Tana 2015). The Russian stock market plunged. By December 2014 the RTS index stood at about 700, a fall of two-thirds from its value in 2011. Inflation surged; in March 2015 it reached a rate of 16.9% per year, and it remained above 15% until December (Tanas 2015). Even more dramatically, the Russian ruble seemed near collapse. On December 16, 2014, a euro cost 91.5 rubles (European Central Bank Statistics). This had two further negative effects for Russia. First, the government began to run down its hard currency reserves in an attempt to support the ruble. The government spent almost 40%of its liquid reserves from July 2014 to April 2015 (DeFotis 2015). And second, in a desperate bid to induce investors to keep money in the country, interest rates were raised sharply, leaping from 10.5 to 17% near the end of 2014. This seemed to have little immediate effect on capital flows, but did further harm struggling Russian businesses. In the few sectors which could potentially benefit from the ‘sanctions war’ with the West—for example, domestic producers of high quality foodstuffs, which Moscow now refuses to buy from Europe—businesses found it almost impossible to secure financing. In short, Russia was suffering from ‘stagflation,’ a dangerous combination of high inflation and falling GNP.

Russia’s condition seemed to stabilize somewhat after 2015, although the country remained much weaker economically than before sanctions were imposed. Interest rates had fallen to 11% by the end of 2015, and 9.25% by April 2017. However, the medium-term prognosis remains weak. For example, the net profit reported by Gazprom fell 86% from 2013 to 2014 (2015, ‘Gazprom profits hit by weak rouble,’ BBC News, 29 April). The stock market fell again, before recovering somewhat. The RTS index stood at 736 on January 6, 2016, before rising above 1000 by early 2017. Similarly the ruble, which had recovered somewhat by mid-2015, fell again later in the year. By January 2016 it stood at levels similar to those seen in the crisis of December 2014. Although it has gradually recovered since then, it has still lost about half its value compared to pre-crisis levels. Thus it is clear that the sanctions (along with declines in oil prices) have had an effect, imposing costs on Russia and thus weakening its ability to project economic power in its own right. For example, with depleted foreign currency reserves, the country is less able to offer loans to favored states, and with Gazprom losing profitability, it is less able to manipulate prices for political reasons. Such results can be considered a ‘success’ by those favoring sanctions.

Finally, we must consider the third factor in the sanctions’ impact: will they affect President Putin’s domestic popularity? There is some evidence that this has begun to happen. Other political parties in Russia’s tightly controlled ‘bloc party system,’ in which the "opposition" parties almost always vote with Putin, have begun to balk in some cases. In October, 2014, for example, Putin was barely able to get the normally-compliant Russian Parliament to pass a bill compensating rich oligarchs whose overseas property was expropriated by Western sanctions. The vote was only 232-202, with all parties other than Putin’s United Russia voting against. This unexpectedly strong opposition was linked to resentment over the fact that economic problems could lead to cuts in popular programs, such as government grants given to families having children. One Liberal Democratic Party lawmaker was quoted as saying 'why should we compensate people with yachts on the Côte d’Azur when we can’t support unborn children?' (Rudnitsky & Meyer 2014)

The Russian people, too, are beginning to raise questions as economic pressure grows. For example, some Russian companies—and the state itself—have now returned to a deeply unpopular tactic rarely seen since the Yeltsin years: delaying payment of workers’ wages, sometimes for months. As an April 2015 article in The New York Times documented, desperate workers scattered across the country—from teachers in the Far East to autoworkers near the Estonian border—had begun to launch small-scale strikes and protests over this issue (Kramer, 2015). When economic decline reaches this point, political discontent seems likely to rise, eventually. Recent opinion polls in Russia have reflected this change. Putin’s party, United Russia, was favored by about 45% of voters before the 2014 crisis. In spring and summer of 2014 this jumped suddenly to about 60%. However, it has since drifted downward, and as of May-June 2016 had returned to about 45% (Russian Public Opinion Research Center). Nonetheless, United Russia was still able to prevail in the Duma elections held in September, 2016. Clearly, some of the ‘rally round the flag’ effect predicted by Galtung (1967) and Eland (1995) remained.

Russian Economic Power and Ukraine

The West, then, has significant economic leverage which it can use to influence both Ukraine and Russia. Yet unlike in many past cases of sanctions, Western nations here face an opponent who can fight back—militarily and economically—both against Ukraine and against the West itself.

As many observers have noted, Russia’s most important economic tool is its control over the energy supply of its neighbors, especially through natural gas exports (Stuhlberg 2007; Goldman 2008; Newnham 2011b). Yet Russia has many other tools at its disposal; for example, like the West, it can offer financial credits and raise or lower its trade barriers. As we shall see, many of Russia’s neighbors—including the E.U. states as well as Ukraine—have some degree of dependence on Russia as an export market, which the Kremlin can exploit.

Ukraine has lived with the reality of Russia’s economic influence since it became independent at the end of 1991. Since the Russian economy is over ten times larger than Ukraine’s, any given economic sanction (or incentive) is relatively much cheaper for Moscow than Kyiv.12 Accordingly, the Russians have continually tried to use economic levers to either promote friendly governments or punish unfriendly ones. The shifting winds from the Kremlin have been clear. Before 2004, President Kuchma was seen as relatively pro-Russian. Thus, for example, Ukraine was able to buy natural gas for only about $50 per thousand cubic meters (TCM) and was able to export freely to Russia, shipping many uncompetitive manufactured goods and agricultural products. Ukraine’s accumulated debt to Russia was pursued in only a desultory fashion. Suddenly, however, with the Orange Revolution bringing the pro-Western Yushchenko government to power, the Kremlin turned hostile. Gas prices soared by a factor of five, to about $250 per TCM. “Customs problems” mounted for Ukrainian goods. And debts were pursued fiercely. Most dramatically, Moscow cut off Ukraine’s gas supply twice, in 2006 and 2009, both times in the depth of a cold northern winter. As I have argued elsewhere, Russian economic pressure played an important role in wrecking Ukraine’s economy at this time, helping to pave the way for the election of the relatively pro-Russian President Victor Yanukovych in 2010 (Newnham 2013).

Yanukovych soon was rewarded by the Kremlin. He quickly signed an agreement with Moscow extending the Russian Navy’s lease on key bases in the Crimea, which Yushchenko had long resisted. In return, the Russians immediately cut Ukraine’s gas cost by 25% (Levy 2010). Pressure to pay past debts eased, and access to the Russian export market improved. However, when the Yanukovych regime announced in 2013 that it would sign an Association Agreement with the E.U., the economic temperature suddenly cooled again. No stone, large or small, was left unturned. For example, ‘chocolate Czar’ Petro Poroshenko—at the time merely a prominent Ukrainian businessman—found that his products were unwelcome in Russia, due to alleged quality issues, including contamination with carcinogenic chemicals (Flintoff 2014). Many other threats were reportedly made—for example, that Ukrainians might lose the right to work in Russia. And in August 2013, Moscow tightened enforcement of every trivial customs rule it could find, delaying or rejecting many trade shipments from Ukraine (2013, ‘Ukraine and Russia: trading insults,’ The Economist, 24 August). Yet when Yanukovych suddenly decided to skip the November 2013 Vilnius summit with the E.U., refusing to sign the planned Association Agreement, the Kremlin again instantly warmed to him. Poroshenko, for example, was told that all difficulties experienced by his factories would end quickly. On a grander scale, the Kremlin quickly negotiated a 'Ukraine-Russia Action Plan' with Yanukovych, offering a variety of economic incentives. The tightened customs rules imposed in August were abruptly dropped. Gas prices were further reduced, from a rate then above $400 per TCM to $268. And most importantly, a loan of some $15 billion was offered, although only $3 billion was provided immediately (McElroy 2013).

When the Yanukovych regime fell in February 2014, Russia’s economic incentives again morphed instantly into economic sanctions targeting the new, pro-Western government. Russia refused to pay out the remaining $12 billion in loans which it had offered Yanukovych only two months earlier. In fact, it has demanded immediate repayment of the $3 billion which had already been disbursed (Schearf 2015). Kyiv also quickly faced trade sanctions and even the outright seizure of Ukrainian assets in Russia. Outspoken political opponents of the Kremlin were singled out for particularly harsh treatment. For example, Petro Poroshenko, now President of Ukraine, saw his Roshen candy factory in Russia face a series of legal actions, culminating in a police raid and the court-ordered seizure of the entire business, allegedly for tax violations (Yakovenko 2015).

Russia also resumed the use of its most potent weapon, its control of Ukraine’s energy supply. Moscow again drastically increased the cost of Ukraine’s natural gas. First, it cancelled the 25% reduction linked to the lease renewal for Crimean naval bases. With the seizure of Crimea in March 2014, Russia claimed, that agreement was now null and void. Next, Moscow threatened to vastly increase even that price, demanding almost $500 per TCM, far above the rate charged to even the wealthiest West European countries. In the ten years since 2004, then, Moscow had raised the gas price ten-fold—from about $50 to $500 per TCM. In addition to the vast price increases, Moscow also demanded immediate cash payments of all accumulated energy debts. Alleging that Ukraine might not pay for gas after delivery, the Russians also asked for advance cash payment for any future shipments. These conditions had never been demanded of the Yanukovych government. When Kyiv would not comply immediately, Moscow simply turned off the country’s gas supply, on June 16, 2014—and left it off (Walker 2014). This time, the embargo was to last not for a few days, but for four long months.

In the end, the threat of a ‘cold winter’ for Ukraine was avoided at the last minute, as the E.U. was able to broker a deal with Russia on Ukraine’s gas supplies. The deal which was finally reached on October 30, 2014, called for Kyiv to pay from $268.50 to $378 per TCM for various parts of its winter supply. This was a painful increase from the roughly $250 it paid when Yanukovych ruled the country, although less than the nearly $500 price initially demanded by Moscow (Kanter 2014). And to make matters worse, Russia still insisted on payment of past gas debts; it was to receive $3.1 billion by the end of 2014 for debt payment, in addition to about $1.5 billion for current supplies. With Ukraine relying on foreign loans, the West ironically found itself effectively paying Moscow for Ukraine’s gas. By supplying almost $5 billion to Russia, the deal also significantly undercut the Western sanctions policy.

This episode is a good example of how advocates and opponents of sanctions can view the same incident differently. While some focus on the harshness of Russian policy in the unprecedented four-month gas embargo, others such as Adam Stulberg (2015) stress that the Kremlin ultimately showed restraint by agreeing to a compromise solution. And the question of Russia’s motivation remains open. Part of it was certainly that the pain from Western sanctions was already beginning to be felt, and Gazprom (and Russia as a whole) needed the payments associated with the deal. At the time, Russia’s Energy Minister, Alex Novak, stated that Russia was acting 'to show it was a reliable commercial partner for the E.U.,' likely hoping that this might help to motivate the E.U. to show similar flexibility by rescinding its sanctions (Kanter 2015).

In all, though, Russia’s sanctions—and military action—against Ukraine have had a devastating effect on the country. As noted earlier, Ukraine’s economic growth slowed down, dropping by an estimated 6.6% in 2014 and 9.8% in 2015 before a slight recovery in 2016 and 2017 (CIA World Factbook: Ukraine Economy). Inflation was estimated at 48.7% for 2015, a crippling rate. And the government struggles to borrow enough to stay afloat. The economic problems are very ominous for the Poroshenko government. While the government did briefly enjoy popular support, in a patriotic response to Russia’s invasion of Crimea and Eastern Ukraine, it has had difficulty maintaining this as the economy slides. By late 2016 Poroshenko’s approval rating was abysmal. For example, in a poll reported in November in the Kyiv Post, 73% of respondents had an unfavorable view, with only 20% favorable (2016, ‘Survey Shows Poroshenko Not Supported by 73% of Ukrainians,’ Kyiv Post, 2 November). As noted above, Russian sanctions and the resulting economic problems played a role in discrediting President Yushchenko and the Orange Revolution, helping to lead to his electoral defeat in 2010 (Newnham 2013). The Kremlin now seems to hope that history will repeat itself.

Russian Economic Power and the West

From the beginning of the Ukrainian crisis, Russia made it clear that any Western economic sanctions would be met with retaliation. In fact, Moscow had already sanctioned some individual American citizens after the U.S. passed the Magnitsky Act in 2012. 13With each stage of the Ukrainian crisis, Moscow’s list of sanctioned individuals grew, encompassing not only Americans but a number of Europeans. It now includes, for example, 89 prominent European political leaders, some of whom have been stopped at airports and denied entry into Russia (2015, ’89 European political and military leaders banned from Russia,’ The Guardian, 30 May).

The E.U. was also threatened by possible interruptions in its supply of Russian natural gas. Unlike Ukraine, the E.U. could pay its bills. But it still faced possible Russian gas sanctions, for two reasons. First, in its effort to evade Moscow’s gas sanctions, Ukraine could supply its own needs by siphoning gas in transit to the E.U., as it had done in gas disputes with the Kremlin in 2006 and 2009. This could not only directly impact the E.U. by reducing its supply; it could lead to Moscow cutting the amount of gas put into the pipelines to discourage siphoning. Thus, if siphoning continued, the amount reaching the E.U. could fall even further—possibly to zero. However, there was also a second reason for the E.U. to fear gas sanctions—the issue of reverse gas flows. In an effort to help Ukraine, several E.U. countries had resold Russian gas to Kyiv, starting in summer 2014 when Russia cut off the Ukrainian supply. Since resold gas helped Kyiv to resist the Russian embargo, Moscow frowned on this practice. As a result, within a short time mysterious temporary supply cuts were felt by such countries as Poland (DeFotis 2014) and Slovakia (Carney 2014). While Russia did not confirm this, many observers believed the cuts were carefully calibrated signals, warning these states that if reselling continued they could face full-scale gas embargoes.

However, the main area which Moscow targeted with its sanctions was food products. For many years the Kremlin had used this "food weapon" against former Soviet states, which it wished to punish. For example, Georgia had been targeted for years with sanctions against its wine and mineral water producers (Newnham 2015). Now the same method was turned against the E.U. and other Western states. In October 2013 Moscow halted imports of dairy products from Lithuania. This measure was officially for 'safety reasons,’ but was universally seen as punishment for that country’s decision to host the November summit at which Ukraine, Moldova and Georgia were to sign the E.U. Association Agreements. As the Ukraine crisis deepened in 2014, the food weapon was again trotted out. In January, all pork imports from the E.U. were stopped, allegedly because of disease concerns. In July, Poland—one of Russia’s strongest critics in the E.U. – was informed that its lucrative fruit and vegetable exports to Russia would be stopped. However, the most serious counter-sanctions were announced on August 6, 2014, just after the West imposed its ‘Phase 3’ sanctions, detailed above. The Kremlin decided to cut off most food imports from all Western states participating in ‘Phase 3.’ This included not only the E.U. and US, but also Norway, Canada, and Australia. These sanctions have been renewed regularly since then, most recently in June 2016, at which time they were extended until the end of 2017.

Impact of Russian Sanctions on the West

As was the case with the Western sanctions against Russia, the effects of these sanctions will now be considered in three areas: their economic impact, their effect on the domestic politics of the targeted states, and their impact on the foreign policy of the West.

The economic impact of these sanctions varied. The U.S. exported $1.3 billion in agricultural products to Russia in 2013, while the E.U. exported $15.8 billion (2014, ‘Russia hits West with food import bans in sanctions row,’ BBC News, 7 August). For some Western states, such as the U.S., the impact of Russian counter-sanctions seemed small. Since overall U.S. exports were $1.575 trillion in 2013, including $145 billion in agricultural products, the sanctions would affect less than one percent of agricultural sales and a miniscule 0.08% of total U.S. exports (CIA World Factbook). However, for some countries, especially in Western Europe, the losses loomed much larger. Norway, for example, faced the loss of its largest purchaser of fresh seafood—accounting for $1.06 billion in annual sales—a significant blow to an economy only about three percent as large as the U.S.’ (Tallaksen 2014). For countries with weak economies, the loss of exports was even harder to bear. Greece, for example, looked to Russia as an important market for fresh fruit exports. Given the state of its economy, even small economic losses loomed large politically. And Lithuania, an agricultural country traditionally linked to the Russian market, faced the worst blow of all—2.5% of its GDP was reportedly made up of sanctioned products. (2014, ‘Russia hits West with food import bans in sanctions row,’ BBC News, 7 August). Particularly upsetting for the Europeans was the fact that many of the affected exports—such as fruit, seafood, and cheese—were highly perishable. Thus, in the short term, it was well-nigh impossible to find alternative buyers. When the Russian boycott was suddenly imposed, trucks were literally turned away at the border with nowhere to go.

The Russians, then, like the West, were wise enough to use ‘smart sanctions,’ targeting their opponents’ most sensitive economic sectors. It must also be remembered that the agricultural sector has huge political clout in Western Europe, as President Putin was well aware. Thus, it no doubt seemed plausible to the Russians that agricultural sanctions would lead to a speedy outcry from farmers, and perhaps to concessions from the E.U. Indeed, the E.U. did respond very quickly to placate the farmers. Within days of the Russian action it offered special agricultural financing, amounting to about $167 million (Ruitenberg 2014). European leaders tried to promote a ‘buy local’ campaign. For example, the German agriculture minister, Christian Schmidt, promoted German apples with the slogan “An Apple a Day Keeps Putin Away” (2014, ‘An apple a day keeps Putin away,’ Der Spiegel, 27 August).

Threats to areas such as agriculture and energy, however, are far more than sectoral problems: they can drag down the whole E.U. economy. This gives Russia’s counter-sanctions much more impact. The E.U. is vulnerable to these sanctions, because its economy, while large, has been mired in recession since 2008. Facing slow or no growth at home, the E.U. had looked to exports to buoy itself—and was starting to make some progress. Russia’s sanctions, while not all-encompassing, have helped cause the E.U.’s recovery to stall. The E.U. itself estimated that the conflict with Russia would cost it 0.2% in regional GNP in 2014, and 0.3% in 2015 (Norman 2014). This economic slowdown is far less than that faced by Russia. As noted above, the Russian economy fell by almost 4% in 2015.

However, even a small downturn can have a strong domestic political impact on the E.U. and its partners, since the Western states are democracies. And as was discussed in the theory section of this paper, studies have shown that democratic states may be more vulnerable to sanctions, since affected sectors can quickly and easily react politically to any economic pain. Dissent can be voiced very cheaply, without consequences (in contrast to the situation in Russia), and dissenters are easily able to support alternative political parties and vote them into office.

This has proven the case in the E.U., for example. First, dissent over the ‘sanctions battle’ with Russia has been quite visible. For example, both farmers and business leaders linked to the Russian market have spoken up forthrightly. They first opposed the sanctions as they were being imposed, then began to lobby for them to be lifted if Russia made even minimal concessions. Germany, for example, saw its exports to Russia fall by almost half, from 38 billion Euros in 2012 to only 21 billion in 2015, with a further 10% drop in 2016 (2016, ‘German exports to Russia set to fall to ten year low,’ AFP, 19 February). It is thus not surprising to see that the President of Siemens would meet with President Putin even as his country was imposing sanctions on Russia, and that leaders of companies such as Adidas and ThyssenKrupp would echo his concerns (Czuczka 2014). Similarly, former Chancellor Gerhard Schröder—now chairman of the German-Russian gas pipeline company Nord Stream—said that Russia’s land grab in Crimea was just as legitimate as Kosovo’s secession from Serbia, echoing the Kremlin’s line (Paterson 2014). Schröder has continued to lobby for the Russian viewpoint in Germany; for example, he was among the few prominent Westerners to attend the St. Petersburg Economic Forum in June 2015, at which Putin delivered a blistering attack on Western policy.

Finally, then, have Russian sanctions had an impact on Western foreign policy? This seems to many to be most likely in the E.U. The E.U. has a very unwieldy decision-making model, in which all 28 member-states must consent to important policies. Observers were very impressed that the Union managed to agree on three rounds of sanctions—this is an achievement. The Union was even able to maintain unanimity in renewing the sanctions for a further six months in both June and December of 2015 and 2016. However, the E.U. now faces the harder task of maintaining that solid front for an indefinite time in the face of Russian intransigence. If even one state defects from the policy, sanctions cannot be maintained. And a number of states are buckling.

Within a few weeks of the imposition of ‘stage three’ sanctions, some states in the Union were sounding dissonant notes about how long they should last and when they should be lifted. The election of the seemingly pro-Russian Tsipras government in Greece in early 2015 strengthened the dissension. Tsipras hastily visited the Russian embassy soon after his victory. He followed up with two trips to Russia in his first few months in office, asking the Kremlin to give Greece loans and exempt it from Russia’s sanctions on Western food exports (Hille & Weaver 2015). In addition to Greece, a number of other E.U. states are questioning the sanctions policy. Cyprus, for example, has long hosted a number of Russian banks and corporations. Bulgaria, too, has extensive economic ties with Moscow, and has also long been seen as pro-Russian politically, from the days when Russia helped to create the country after its wars with Ottoman Turkey in the late 1800s. Like Greece, Cyprus and Bulgaria also share the Orthodox faith of Russia, and thus often sympathize with the Kremlin’s worldview. Italy and Spain, both distant from Ukraine and both among the Union’s laggards economically, are also seen as sympathetic to lifting sanctions. Like the struggling Greeks, even a small boost to their economies would be of great political importance for their governments. Hungary, too, under its Euroskeptic leader Viktor Orban, has loudly questioned the need for ongoing Western sanctions (Byrne 2017).

In the most direct vote yet in the West on Ukrainian policy, the voters of the Netherlands on April 6, 2016, voted against the E.U.’s Association Agreement with Ukraine. Opponents of the agreement were able to force an advisory referendum on it. With a low turnout of only 32.28%, they were able to receive 61% of the votes, with only 38.2% of voters favoring the accord (2016, ‘Dutch referendum voters overwhelmingly reject closer E.U. links to Ukraine,’ The Guardian, 7 April). Opponents argued the agreement was too costly to the Netherlands, opening the country to more economic competition and more migration from Ukraine. While this vote did not directly concern the E.U.’s sanctions policy, it was an ominous sign that support for Ukraine was weakening.

Thus far, the smaller Western countries have reluctantly gone along with continued sanctions, but this may not continue. And ominously, larger states are now also weakening in their commitment. As predicted in the theory section of this paper, elections are vulnerable points for democracies, where new leaders can exploit economic grievances to come to power and change a country’s foreign policy. Recently three such elections in major Western countries have shaken the West’s commitment to defending Ukraine with sanctions.

First, in the summer of 2016, the world was shocked by the ‘Brexit’ vote, as Britain voted to leave the E.U. This vote was driven by white working-class voters who were uneasy about economic decline and an influx of immigrants. Ukraine did not seem to be a major issue in the campaign directly, but some Brexiteers, like the Dutch, condemned the E.U. agreement with Ukraine as being costly to the British economy and opening the door to more immigration. The Brexit vote may have a serious impact on the Union’s sanctions policy, since Britain has in the past been a strong advocate of sanctions. Even if its government does not change its views, by leaving the Union, Britain will weaken the pro-sanction forces in the E.U. A recent House of Commons report notes that after Brexit 'it may be increasingly difficult to sustain a unified Western position on Ukraine-related sanctions' (Reitman 2017).

Second, in November 2016 the world was stunned again by the election of Donald Trump in the U.S. His support, like that of Brexit, was driven by working-class white voters who felt left behind economically and were eager to support any policy which promised to bring more jobs. Trump was quite open in his desire to improve relations with Russia, and both he and many of his allies questioned sanctions. In January 2017, for example, he hinted at finding a way to revoke sanctions, stating 'they have sanctions on Russia—let’s see if we can make some good deals with Russia' (Gordon & Chokshi 2017).

Finally, in spring 2017 the E.U. had a close call in a third vital election, for the President of France. Marine Le Pen, the National Front candidate, was stridently pro-Moscow, calling loudly for the end of sanctions on Russia and the acceptance of Russia’s annexation of Crimea (2017, ‘France’s Marine Le Pen urges end to Russia sanctions,’ BBC News, 24 March). Economic stagnation in France allowed her to mobilize the same sort of working-class voters who had backed Brexit and Trump. The National Front, formerly a fringe movement, thus was able to come within striking distance of victory. The E.U. leaders openly feared that a victory for Le Pen would bring an end to sanctions on Russia, since France would be a strong enough player to openly veto the expected sanctions renewal in June 2017 (Baczyska 2017). While Le Pen fell short in the final run-off election on May 7 against the moderate candidate Emmanuel Macron, it was stunning that she was able to make it that far, achieving her party’s best showing in history.

With each election, it seems, the ‘sanctions fatigue’ in the West grows, and the risk of the West making concessions on Ukrainian issues increases. President Putin and his minions will be sure to remind Western leaders at every opportunity that sanctions are costly to their economies. As shown in the theory section of this paper, every 1% decline in a democratic country’s economy results in a roughly 2% decline in the vote share of an incumbent party. This fact makes it difficult for Western countries to keep pace in a ‘sanctions battle’ with an opponent like Moscow, who is willing to fight back strongly.

Finally, another problem is perhaps even bigger for the E.U. and for the West in maintaining its policies in the ‘sanctions battle’ with Moscow: its commitment to Ukraine is limited. The issue is not central to many Europeans—to say nothing of Japanese, Australians, and Americans—in the same way it is to Russians.14 This gives Moscow an advantage in its struggle with the West over Ukraine: although the West can impose higher costs on Russia than Russia can on the West, the West may not be willing to bear even limited pain. As the British Prime Minister Neville Chamberlain infamously said in 1938, when he allowed Hitler to dismember Czechoslovakia, 'why should we go to war for a faraway country about which we know nothing?' Many in the West may quietly feel the same about today’s ‘economic war’ with Russia over Ukraine. Until now Western unity has been maintained, but the Kremlin has good reason to think that in the medium term it may begin to buckle.

Conclusion and Policy Recommendations

As this paper has made clear, evaluating real-world cases of economic linkage today can be complex. This is true both for the sanctions’ economic impact as well as their political and foreign policy impact. First, a central point of this article is that sanctions may not be one-sided. Two powers may both be employing sanctions in opposition to each other. Second, the sanctioning powers may be targeting multiple countries. In this case, for example, both the West and Russia were targeting not just each other but Ukraine as well. And Russian sanctions had a very different impact on different Western countries, with some (like the U.S.) feeling little pain, while others (like Norway and Lithuania) were seriously affected. Again, this is rarely studied in the existing sanctions literature, which tends to focus on the impact of sanctions on one target state. Third, sanctions may encompass a number of different instruments. Thus one cannot focus only on trade sanctions or only on financial instruments, as many authors do, but must look at many areas to truly gauge a policy’s impact.

Once an observer has estimated the economic impact of sanctions, however, the task is not over. What is the political impact of the sanctions? Here too, the existing literature has oversimplified matters. Most studies simply ask, 'has the target given up?' If that state has not radically changed its offending policies, the sanctions are rated as a failure. But should this be considered a yes/no question? One must ask, would the target have taken more extreme actions without the sanctions? And have they softened the target’s negotiating stance in any way? These questions may be harder to answer. Sanctions supporters argue that Russia could easily have conquered all of Ukraine, as Putin threatened. Yet it shrank back from such a dramatic break with the outside world. Putin agreed to a ceasefire in Minsk in September 2014, and he conceded the legitimacy of the hated Poroshenko government and the new pro-Western parliament elected in October. An optimist would say that this left Russia as the loser in Ukraine, as it was effectively conceding most of the country to the West. However, sanctions opponents argue that Putin’s ‘concessions’ are purely cosmetic. In their view, he has basically won. He has clear possession of Crimea, with even some of his few remaining domestic critics conceding the point.15 And the conflict in Eastern Ukraine seems to have frozen in place, giving Putin a permanent pressure point to use against the beleaguered government in Kyiv.

What can the Ukrainian sanctions case tell us about broader issues in international relations? I would argue that this case is likely to be typical of the new world we increasingly face. The existing sanctions model is based on an outdated world view from the 1990s. It assumes the U.S. will remain the world’s leading economic power, and will have the ability to impose powerful unilateral sanctions. The only question asked by this literature is whether Washington can be even more effective by inducing other Western countries, and even the UN, to join it in imposing multilateral sanctions. On the other side, the target country is presumed to be relatively isolated and economically weak—like Cuba, Serbia, North Korea or Iraq under Saddam Hussein. At best the only help it can expect is from a few economically motivated ‘sanctions breakers.’

Today, though, we face a different world. With the rise of the BRICS states (Brazil, Russia, India, China, and South Africa), the West no longer has a monopoly on economic power. It can face economically powerful opponents. Thus, the U.S. and its allies may face two unpalatable kinds of cases. First, they may be attempting to target an economically powerful opponent, much better able to resist than the weak pariah states targeted in the past. Or second, they may be targeting a weaker state, only to find their efforts blocked by one of these powerful new opponents. The Ukrainian case is interesting, since it has elements of both problems. First, the West has found it difficult to successfully undermine Russia economically, since Russia has an economy which is both fairly large—and thus resistant to sanctions—and also has countervailing economic power which it can use for retaliation against the West. And second, as we have seen, Russia can also use its resources to counter Western efforts to help Ukraine.

As the new BRICS grouping symbolizes, these rising economic powers may cooperate to oppose Western sanctions, making success against any one of them even more difficult. In the current Ukrainian case, for example, China has seemed to support Russia in several ways. The two countries signed a major agreement on natural gas sales, offering Russia a new market in case sales to Europe fall (Weitz 2014). Chinese companies are also often willing to displace Western investors in Russia (Rapoza 2015). Countries such as Brazil and India, while playing a smaller role, have been happy to replace the West in supplying food and other exports to Russia, and have also offered some investments (Phillips 2014; Pearson 2014).

Additionally, as this case has shown, the West faces another problem: both the countries it supports (like Ukraine) and the West itself are generally democracies. The countries it is competing with generally are not. And, as seen in this case and in the broader literature, democracies may be more vulnerable to economic sanctions. Since voters can easily and "cheaply" turn out democratic leaders, a small economic downturn may hurt the West, while autocratic leaders can withstand similar pressure.

Who will win out in this case? As we have seen, Russia is suffering economically, but as yet shows few signs of policy change. Meanwhile, the West is suffering less, but may lack the political will to continue the contest. And its ally Ukraine is faring even worse economically than the Russians. Who will falter first? The final outcome of the Ukrainian case remains uncertain, and its result will reveal much about the balance of economic power in today’s new, more multilateral world.

Nonetheless, this study also shows that the West should not despair. How, then, can the U.S. and its allies respond to this challenging new environment? I would suggest three areas of policy recommendations which could help the West to continue to use economic sanctions effectively even as ‘sanctions battles’ become more common.

First, Western policymakers should continue to use and refine the ‘smart sanctions’ approach, as discussed in the work of authors such as Cortright and Lopez (2002) and O’Sullivan (2003). This will serve to maximize the bloc’s slowly declining economic clout in world affairs. Rather than imposing blanket embargoes on targeted countries, the West should target sanctions based on three factors. First, what are the economic sectors where the target is most vulnerable? Second, what are the sectors where the West has the greatest economic power? And third, how can sanctions be structured to impact ruling elites, while minimizing ‘collateral damage’ to civilians? All of these tactics could be seen, for example, in the Western technology sanctions against the former Soviet Union. Forbidding Moscow to purchase computers and other advanced technology was effective, since the USSR was rather backward in these areas while the U.S.—along with its European and Japanese allies—controlled most world production of these products at the time. Also, these products were vital for high-priority state projects in military and other areas, but were not seen or used by the average Soviet citizen. In contrast, the West generally allowed exports of food and other consumer goods to the Soviet Union—except for the short-lived and unpopular Carter grain embargo. This allowed America and its allies to portray themselves as sympathetic to the common people of the USSR, which may be one reason why many Russians viewed the West in a fairly favorable light as the Soviet Union collapsed.

Similarly, as shown in this paper, it could be argued that the sanctions against today’s Russia over the Ukrainian crisis have also been relatively ‘smart,’ although, in this case, the vulnerable sectors are different. Russia today is a capitalist state, albeit one dominated by a small group of politically-connected cronies of President Putin (Dawisha 2014). Thus, rather than focusing only on technology, the West has used financial sanctions directed against certain individuals and companies. And with Russia now relying on oil and gas exports, the West has also targeted investment and some specialized technology in that sector. Again, the average Russian is not directly affected. In fact, it could be argued that Putin’s regime has harmed the average Russian more, by targeting Western food exports for retaliatory sanctions. This has resulted in a dramatic rise of food prices, which is very visible to Russian consumers.16

Second, as its own economic power slowly falls in relative terms, the West needs to put more emphasis on coordinating sanctions among many actors. The first priority should continue to be coordination between the U.S., E.U., Japan, and other traditional allies. The E.U.’s economy is comparable in size to that of the U.S. Together, the two control over 35 trillion dollars in GNP, dwarfing even the economy of China (about 10 trillion), let alone that of Russia (2 trillion). Adding Japan, Australia, and Canada brings the Western total to some 43.5 trillion. 17 If the West can remain united, it can exploit its still-strong role in some sectors, such as finance. The West still has disproportionate strength in finance, with its control over most of the world’s leading reserve currencies, the dollar, euro, yen, and pound, and most of the world’s large banks and stock markets.18 Additionally, coordination among these countries—while not always easy—remains quite possible, since they largely share common values and priorities in international relations. This has been seen in the recent sanctions against Russia, where, thanks to patient diplomacy, the West has remained united in opposing the Kremlin.

Additionally, the U.S. must strive to involve even more countries in its dominant economic coalition, notably the rising BRICS powers. While this can be difficult, it is not impossible—as the sanctions imposed against Iran by the United Nations demonstrate. China and Russia joined the U.S. and the E.U. in sanctioning Iran, and joined the Western powers in negotiating with Tehran to curb its nuclear ambitions. While the deal reached with Iran is certainly not perfect and its future remains uncertain after U.S.' withdrawal, it can be argued that it is better than anything the West could have achieved on its own.

Finally, if necessary, the U.S. should remember that it can still sanction unilaterally with some effectiveness, especially when targeting small states and those without powerful outside patrons. The 18 trillion dollar American economy dwarfs that of most states. For example, in 2016 only 15 countries in the world had economies above one trillion dollars.19 America’s status as the world’s leading importer makes access to its market a valuable lure.20 And it continues to be the world’s leading aid donor.21 Thus, while acting in concert with others is certainly preferable, especially as America’s relative economic position slowly weakens, it should still be able to use unilateral sanctions in many cases for some time to come.

Randall E. Newnham is a Professor of Political Science at Penn State Berks. He can be reached at ren2@psu.edu. [1]

References

Adekoya, R 2014, ‘How the EU transformed Poland,’ The Guardian, 1 May. Available from: https://www.theguardian.com/commentisfree/2014/may/01/eu-poland-10-years-economic [2].

Ahmed, S 2015, ‘Vladimir Putin’s approval rating? Now at a whopping 86%,’ CNN.com, 26 February. Available from https://www.cnn.com/2015/02/26/europe/vladimir-putin-popularity/index.html [3].

Baczynska, G 2017, ‘EU on course to renew Russian sanctions barring Le Pen win,’ Reuters, 28 April. Available from: https://www.reuters.com/article/us-ukraine-crisis-eu-russia-idUSKBN17U1D6 [4].

Baker, P 2014, ‘U.S. expands sanctions, adding holdings of Russians in Putin’s financial circle,’ The New York Times, 28 April. Available from: https://www.nytimes.com/2014/04/29/world/asia/obama-sanctions-russia.html [5].

Baldwin, D 1986, Economic statecraft, Princeton University Press, Princeton, NJ.

Bartool, I & Sleg, G 2009, ‘Bread and the attrition of power: economic events and German electoral results,’ Public Choice, vol. 141, nos. 1-2, pp. 151-165.

Blackwill, R & Harris, J 2016, War by other means: geoeconomics and statecraft, Harvard University Press, Cambridge, MA.

Borger, J, Lewis, P & Mason, R 2014, ‘EU and U.S. impose sweeping economic sanctions on Russia, The Guardian, 31 July. Available from: https://www.theguardian.com/world/2014/jul/29/economic-sanctions-russia-eu-governments [6].

Burns, W 1985, Economic aid and American policy toward Egypt, 1955-1981, SUNY Press, Albany, NY.

Byrne, A 2017, ‘Orban joins Putin in attack on Russia sanctions,’ The Financial Times, 2 February. Available from: https://www.ft.com/content/f1f4482a-e96b-11e6-893c-082c54a7f539 [7].

Carney, S 2014, ‘Russia halves natural gas supplies to Slovakia,’ The Wall Street Journal, 1 October. Available from: https://www.wsj.com/articles/russia-halves-natural-gas-supplies-to-slovakia-1412177795 [8].

Carter, R & Cole, D 2015, ‘G-7 warns Russia of more sanctions, pledges climate action,’ AFP, 8 June. Available from: https://www.news.com.au/world/europe/g7-summit-world-leaders-warn-russia-pledge-climate-action/news-story/162668120302255ddafe44986a32461e [9].

CIA World Factbook: Ukraine Economy. Available from: https://www.cia.gov/library/publications/the-world-factbook/geos/up.html [10].

Copeland, D 2014, Economic interdependence and war, Princeton University Press, Princeton NJ.

Cortright, D & Lopez, G 2002, Smart sanctions: targeting economic statecraft, Rowman and Littlefield, New York.

Council of Europe 2014, Reinforced restrictive measures against Russia, 11 September. Available from: http://www.consilium.europa.eu/uedocs/cms_Data/docs/pressdata/EN/foraff/144868.pdf [11].

Czuczka, T 2014, ‘Siemens CEO rebuked as German business defends Putin partnership,’ Bloomberg News, 30 March. Available from: https://www.bloomberg.com/news/articles/2014-03-30/siemens-ceo-rebuked-as-german-business-defends-putin-partnership [12].

Dawisha, K 2014, Putin’s kleptocracy: who owns Russia? Simon and Schuster, New York.

DeFotis, D 2014, ‘Russia’s Gazprom cuts Polish natural gas supply,’ Barrons, 10 September. Available from: https://www.barrons.com/articles/russias-gazprom-cuts-poland-natural-gas-supply-1410377090 [13].

DeFotis, D 2015, ‘As Russian reserves tumble, strong ruble questioned,’ Barrons, 23 April. Available from: https://www.barrons.com/articles/russia-raises-rate-unexpectedly-shoring-up-ruble-1430403011 [14].

Eland, I 1995, ‘Economic sanctions as tools of foreign policy,’ in Economic sanctions: panacea or peacebuilding in a post-Cold War world? eds. G Lopez & D Cortright, Westview Press, Boulder, CO.

Elliott, K 1998, ‘The sanctions glass: half full or completely empty,’ International Security, vol. 23, no. 1, pp. 50-65.

European Central Bank Statistics, ‘Euro exchange rate to RUB,’ Available from: https://www.ecb.europa.eu/stats/policy_and_exchange_rates/euro_reference_exchange_rates/html/eurofxref-graph-rub.en.html [15].

European Commission DG Development and Cooperation 2014, Support package for Ukraine, 18 July. Available from: http://ec.europa.eu/europeaid [16].

Flintoff, C 2014, ‘Why chocolate is a bargaining chip in the Ukrainian-Russian conflict,’ NPR News, 8 April. Available from: https://www.npr.org/sections/thesalt/2014/04/08/300265710/why-chocolate-is-a-bargaining-chip-in-the-ukraine-russia-conflict [17].

Galtung, J 1967, ‘On the effects of international economic sanctions, with examples from the case of Rhodesia,’ World Politics, vol. 19, no. 3, pp. 378-416.

Goldman, M 2008, Petrostate: Putin, power, and the new Russia, Oxford University Press, Oxford.

Gordon, M & Chokshi, N 2017, ‘Trump criticizes NATO and hopes for ‘good deals’ with Russia,’ The New York Times, 15 January. Available from: https://www.nytimes.com/2017/01/15/world/europe/donald-trump-nato.html [18].

Hille, K & Weaver, C 2015, ‘As Greece teeters, Alexis Tsipras is feted in St. Petersburg,’ The Financial Times, 18 June. Available from: https://www.ft.com/content/1e38db54-15d7-11e5-be54-00144feabdc0 [19].

Hirschman, A 1945, National power and the structure of foreign trade, University of California Press, Berkeley, CA.

Hufbauer, G, Schott, J, Elliott, K, & Oegg, B 2007, Economic sanctions reconsidered, 3rd edn., IIE Press, Washington.

Kanter, J 2014, ‘Ukraine and Russia reach accord on natural gas deliveries,’ The New York Times, 30 October. Available from: https://www.nytimes.com/2014/10/31/business/international/ukraine-and-russia-reach-deal-on-natural-gas-supplies.html [20].

Korb, B & Tanas, O 2015, ‘Russia gets second junk rating from Moody’s on Ukraine, oil,’ Bloomberg News, 20 February. Available from: https://www.bloomberg.com/news/articles/2015-02-20/russia-cut-to-junk-by-moody-s-on-ukraine-crisis-oil-price-fall [21].

Kramer, A 2015, ‘Unpaid Russian workers unite in protest against Putin,’ The New York Times, 21 April. Available from: https://www.nytimes.com/2015/04/22/world/europe/russian-workers-take-aim-at-putin-as-economy-exacts-its-toll.html [22].

Kramer, A 2016, ‘Ukraine makes iffy progress after trade pact with Europe,’ The New York Times, 9 May. Available from: https://www.nytimes.com/2016/05/10/business/international/ukraine-ramps-up-trade-with-europe-but-benefits-are-halting.html [23].

Lektzian, D & Souva, M 2007, ‘An institutional theory of sanctions onset and success,’ Journal of Conflict Resolution, vol. 51, pp. 848-871.

Levy, C 2010, ‘Ukraine extends its lease on Russian naval base,’ The New York Times, 21 April. Available from: https://www.nytimes.com/2010/04/22/world/europe/22ukraine.html?mtrref=www.google.com&gwh=D7D936E7C13EDA1923F956AA3F0A7967&gwt=pay [24].

Mackey, R 2014, ‘Navalny’s comments on Crimea ignite Russian twittersphere,’ The New York Times, 16 October. Available from: https://www.nytimes.com [25]. [9 June 2017].

Markus, G 1988, ‘The impact of personal and national economic conditions on the Presidential vote: a pooled cross-sectional analysis,’ American Journal of Political Science, vol. 32, no. 1, pp. 137-154.

Matlack, C 2014, ‘Putin’s latest target: more than 200 Russian McDonalds,’ Bloomberg News, 20 October. Available from https://www.bloomberg.com/news/articles/2014-10-20/putins-latest-target-more-than-200-russian-mcdonalds [26].

Mayeda, A 2015, ‘IMF approves Ukraine aid package of about $17.5 billion,’ Bloomberg News, 11 March. Available from: https://www.bloomberg.com/news/articles/2015-03-11/ukraine-wins-imf-approval-for-17-5-billion-to-rescue-economy [27].

McElroy, D 2013, ‘Ukraine receives half price gas and $15 billion to stick with Russia,’ The Telegraph, 17 December. Available from: https://www.telegraph.co.uk/news/worldnews/europe/ukraine/10523225/Ukraine-receives-half-price-gas-and-15-billion-to-stick-with-Russia.html [28].

Ministry of Treasury, Republic of Poland 2014, ‘Poland’s economic progress after ten years in the EU.’ Available from: https://www.msp.gov.pl/en/polish-economy/economic-news/5462,Polands-economic-progress-after-10-years-in-the-European-Union.html [29].

Myers, S & Baker, P 2014, ‘Putin recognizes Crimea secession, defying the West,’ The New York Times, 17 March. Available from https://www.nytimes.com/2014/03/18/world/europe/us-imposes-new-sanctions-on-russian-officials.html [30].

Newnham, R 2002, Deutsche mark diplomacy: positive economic sanctions in German-Russian relations, Penn State University Press, University Park, PA.

Newnham, R 2011a, ‘North Korea, Libya, and Iran: economic sanctions and nuclear proliferation,’ Korea Economic Institute Academic Paper Series, vol. 4, 183-202.

Newnham, R 2011b, ‘Oil, carrots, and sticks: Russia’s energy resources as a foreign policy tool,’ Journal of Eurasian Studies, vol. 2, no. 2, 134-143.

Newnham, R 2013, ‘Pipeline politics: Russian energy sanctions and the 2010 Ukrainian elections,’ Journal of Eurasian Studies, vol. 4, no. 2, 115-122.

Newnham, R 2015, ‘Georgia on my mind? Russian sanctions and the end of the Rose Revolution,’ Journal of Eurasian Studies, vol. 6, no. 2, 161-170.

Norman, L 2014, ‘EU projects impact of sanctions on Russian economy,’ The Wall Street Journal, 29 October. Available from: https://www.wsj.com/articles/eu-projects-impact-of-sanctions-on-russian-economy-1414583901 [31].

O’Sullivan, M 2003, Shrewd sanctions, Brookings Institution Press, Washington.

Pape, R 1997, ‘Why economic sanctions do not work,’ International Security, vol. 22, no. 2, pp. 90-136.

Paterson, T 2014, ‘Merkel fury after Gerhard Schröder backs Putin on Ukraine,’ The Telegraph, 14 March. Available from: https://www.telegraph.co.uk/news/worldnews/europe/ukraine/10697986/Merkel-fury-after-Gerhard-Schroeder-backs-Putin-on-Ukraine.html [32].

Pearson, N 2014, ‘Crimean leader seeks Indian investment as Putin visits,’ Bloomberg News, 11 December. Available from: https://www.bloomberg.com [33].

Phillips, D 2014, ‘How Russian ban on US, EU food could turn into a windfall for Brazil,’ The Washington Post, 9 August. Available from: https://www.washingtonpost.com [34].

Rapoza, K 2015, ‘Russia and China are becoming best friends,’ Forbes, 8 May. Available from: https://www.forbes.com/sites/kenrapoza/2015/05/08/russia-and-china-are-becoming-best-friends/#573222806d11 [35].

Razumovskaya, O 2016, ‘IMF raises projection for Russian economic growth,’ The Wall Street Journal, 13 July. Available from https://www.wsj.com/articles/imf-raises-projection-for-russian-economic-growth-1468425424 [36].

Regulation EU No. 374/2014 of the European Parliament and of the Council of 16 April 2014 on the reduction or elimination of customs duties on goods originating in Ukraine. Available from: https://eur-lex.europa.eu/legal-content/EN/TXT/?uri=CELEX%3A32014R0374 [37].

Reitman, A 2017, ‘UK debates post-Brexit Russia sanctions,’ EU Observer, 2 March. Available from: https://euobserver.com/foreign/137079 [38].

Roth, A 2014, ‘Putin tells European official that he could take Kiev in two weeks,’ The New York Times, 2 September. Available from: https://www.nytimes.com/2014/09/03/world/europe/ukraine-crisis.html [39].

Rudnitsky, J & Meyer, H 2014, ‘Russian sanctions compensation bill advances in close vote,’ Bloomberg News, 8 October. Available from https://www.cnn.com/2017/06/15/politics/russia-sanctions-senate-trump/index.html [40].

Ruitenberg, R 2014, ‘EU offers $167 million produce aid after Russia’s ban,’ Bloomberg News, 18 August. Available from: https://www.bloomberg.com/news/articles/2014-08-18/eu-offers-167-million-produce-aid-after-russia-s-ban [41].

Russian Public Opinion Research Center. Available from: https://wciom.ru/news/ratings/elektoralnyj_rejting_politicheskix_partij/ [42].

Schearf, D 2015, ‘Russia’s legal battle for Ukrainian debt fraught with politics,’ Voice of America News, 23 December. Available from: https://www.voanews.com/a/russias-legal-battle-for-ukraine-debt-fraught-with-politics/3115967.html [43].

Shevtsova, L & Kramer, D 2012, ‘What the Magnitsky Act means,’ The American Interest, 18 December. Available from https://www.the-american-interest.com/2012/12/18/what-the-magnitsky-act-means/ [44].

Sonne, P 2014, ‘Russia moves to restrict foreign ownership of media outlets,’ The Wall Street Journal, 28 September. Available from: https://www.wsj.com/articles/russia-moves-to-restrict-foreign-ownership-of-media-outlets-1411760000 [45].

Stuhlberg, A 2007, Well-oiled diplomacy: strategic manipulation and Russia’s energy statecraft in Eurasia, SUNY Press, Albany, NY.

Stuhlberg, A 2015, ‘Out of gas? Russia, Europe, and the changing geopolitics of natural gas,’ Problems of Post-Communism, vol. 62, pp. 112-130.

Tallaksen, E 2014, ‘Norway seafood exports net record year, near $10 billion mark,’ Undercurrent News, 7 January. Available from https://www.undercurrentnews.com/2018/07/05/norway-sets-record-with-first-half-seafood-exports/ [46].

Tanas, O 2015, ‘Russian inflation at fastest in 13 years after ruble crisis,’ Bloomberg News, 6 April. Available from: https://www.bloomberg.com/news/articles/2015-04-06/russian-inflation-at-fastest-in-13-years-after-ruble-crisis.